Key Takeaways

- Bitcoin dominance measures the ratio of the Bitcoin market cap to the cumulative cryptocurrency sector market cap

- It is currently at 58%, the highest mark since April 2021

- Market dynamics are changing as institutions consider Bitcoin, while rest of crypto market still struggles amid tight monetary policy environment

- Regulatory clampdown has also declared many tokens as securities, while Bitcoin appears to be carving out its own niche

The Bitcoin market is never boring.

Having said that, the year 2023 has (thus far at least) has not thrown up mayhem on the scale of what we saw in past years. In 2022, Bitcoin freefell as the world transitioned to tight monetary policy, while scandals such as the Terra collapse and the staggering deception at FTX coming to light. This came after the pandemic years of 2020 and 2021, when crypto surged into mainstream consciousness, Bitcoin printing dizzying gains and inspiring dinner table conversation around the globe as to what this mysterious Internet money was all about.

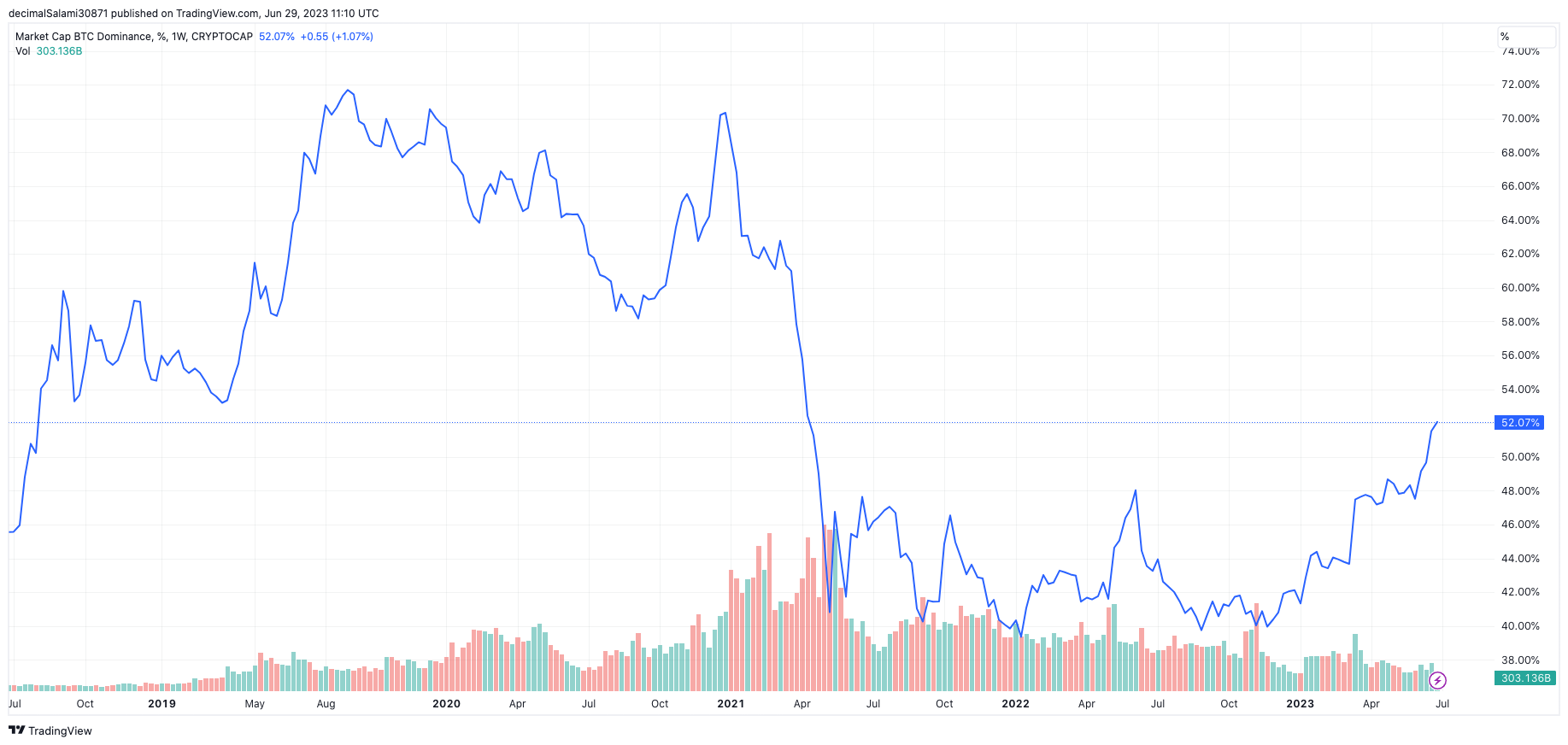

So, 2023 cannot match the scale of that drama. But there is something very intriguing happening to the market dynamics of Bitcoin, at least relative to other cryptocurrencies. Bitcoin dominance, which measures the ratio of the Bitcoin market cap to the cumulative market cap of all cryptocurrencies, is at its highest level in over two years, at 52%. In other words, 52% of the cryptocurrency market cap, currently at $1.18 trillion, is Bitcoin.

![]() Dominance fell in the years 2020 and 2021

Dominance fell in the years 2020 and 2021

Dominance fell in the years 2020 and 2021

Dominance fell in the years 2020 and 2021The above chart shows that Bitcoin opened the year 2020 with a dominance of about 70%. Over the course of the next 365 days, it bounced around a bit and trickled down to the high 50s. However, it was the final quarter of 2020 when Bitcoin began to make serious moves, rising from $10,000 to $28,000. In this time period, the dominance ratio rose from 59% back to 70%, where it closed at, approximately the same dominance ratio it opened the year at twelve months earlier.

The following year, 2021, saw altcoins catch up. Bitcoin’s dominance plunged like a stone, falling quicker than it ever had before. The wider cryptocurrency market exploded as stimulus cheques, lockdown-driven Robinhood trading and basement-level interest rates pushed capital into anything and everything remotely connected to a blockchain.

The total cryptocurrency market cap touched $3 trillion in November 2021, while Bitcoin’s market cap peaked at $1.28 trillion. Bitcoin dominance, therefore, was down to 43%. However, the worst inflation crisis since the 1970s forced central banks into one of the fastest rate hiking cycles in recent memory, following years of zero (or even negative in some cases) rates.

For risk assets, this spelled trouble. And make no mistake, the entire crypto market is as far out on the risk spectrum as it gets. Capital flooded out of the space as rates continued rising, inflation got hotter, and several nefarious scandals struck the crypto sector (looking at you, Do Kwon, Sam Bankman-Fried and Alex Mashinsky).

Which brings us to now. While inflation peaked in Q4 last year, the macro climate is still uncertain. Employment is tight, the economy is still hot and inflation, while dropping, is well north of the Federal Reserve’s 2% target. In Europe, inflation is even hotter (and don’t even ask about the UK, if that still counts as Europe anyway).

In crypto, however, something is changing. Bitcoin’s dominance has risen and appears to be in an uptrend again. It is currently up to 58%, the highest mark since April 2021. On the one hand, this is typical of what we have seen in the past: money begins to flow into Bitcoin after a prolonged and seismic pullback (2022), seeing dominance rise before it eventually filters into altcoins and the rest of the market catches up.

However, there are two points to counter why this time could be different, and may give pause for thought to those assuming that altcoins will follow this time around. The first is, well, obvious: past cycles aren’t indicative of future ones, and this is especially true for Bitcoin.

The asset was only launched in 2009, and it is only in the last five years that it has traded with any sort of reasonable liquidity (although even at that, it’s thin). It would be foolish to put too much weight into previous years, therefore, especially as its entire existence has, until last year, coincided with a remarkable bull market in the wider economy. This is Bitcoin, and crypto’s, first rodeo in a high-interest rate environment, so all bets are off.

But aside from that blindingly obvious caveat, there is more evidence to suggest that there may have been a structural shift with regard to the market in the last six months, or something that may change the dominance trend going forward. What I am referring to is regulation and, more recently, institutional moves.

The regulatory clampdown in the US has been brutal for the crypto sector, with a number of tokens being confirmed as securities by the SEC in recent times, including Solana, Polygon, Cosmos, BNB and Cardano. Bitcoin, on the other hand, appears to be carving out its own niche. Or, as Coinbase CEO Brian Armstrong said when discussing the lawsuit levelled against his exchange by the SEC, “we kind of got this information from the SEC that, well actually, everything other than Bitcoin is a security”.

Therefore, it feels foolish to declare this rise in dominance over the past few months as temporary. If anything, it is surprising that it has not risen more, although a lot of this regulatory trouble may have been priced in already, while the biggest non-Bitcoin token, Ether, seems to have evaded the dreaded security label thus far.

However, there is also the reality of what has been happening on the institutional side in recent weeks. Blackrock and Fidelity, two of the world’s largest asset managers, have both filed for spot ETFs. These are Bitcoin ETFs, not crypto ETFs.

In a sector where regulation is so hazy and the intimidation factor of actually buying physical Bitcoin is so high (the reality is that wallets and seed phrases are not ideal for new users or institutional funds, no matter how seductive the promise of self-custody is), this could do wonders for liquidity – one of the big factors holding Bitcoin back right now. It may also assuage concern around the lack of transparency and reliability of centralised exchanges, as institutions can simply bypass actors like Binance and go straight towards a (regulated) Bitcoin ETF. Of course, these ETFs are not approved yet, but we are a hell of a lot closer to a Bitcoin ETF than any other sort of crypto ETF.

The macro climate is still uncertain: inflation may have peaked but is still elevated, and with monetary policy notoriously operating with a lag, the full pain of a Fed rate north of 5% has yet to be felt. There are numerous challenges still to come. The regulatory crackdown could worsen, while who knows what is going behind the scenes at some of these crypto companies. But it feels undeniable that as bad as things are for crypto, Bitcoin has its head and shoulders above the rest of the gang.

With all this in mind, the rising dominance makes sense. And while I have no idea what happens next (at the end of the day, crypto is going to crypto), I certainly see nothing that would make me confident that Bitcoin dominance, which is now at a two-year high, is bound to inevitably retreat soon.