Crypto’s push for instant settlement is creating a capital inefficiency problem, forcing trading firms to fund every transaction in full and raising concerns about how the market can scale as volumes grow.

In practice, that usually means that firms cannot offset what they owe against what they are owed, forcing them to move more capital than necessary to settle trades.

Ethan Buchman, founder of Cycles Protocol and a co-founder of Cosmos, says crypto markets are “asset-brained.” He argues it treats the financial system like a global stock market where value is constantly moved and swapped.

“But that misses the whole other side of the balance sheet, which is liabilities, and every movement of assets is in service of discharging a liability,” Buchman told Cointelegraph.

Crypto optimized for instant settlement, stripping out the batching and netting that let traditional finance conserve liquidity. At the base layer, that design creates pressure to reintroduce clearing for the industry to scale further.

The logic behind TradFi’s delayed settlement

Clearing is the process of reconciling and netting obligations before settlement, allowing participants to offset what they owe against what they are owed, so only the difference needs to move.

For example, if Alice owes Bob $100 and Bob owes Alice $90, clearing means Alice only pays $10 instead of moving the full amounts both ways.

In traditional financial systems, settlement delays give time to batch and net trades before final payment.

“A lot of people look at T+2 settlement and think it’s inefficient and should be instant — that misses the point. Some of that delay exists to give time for batching and clearing,” Buchman said.

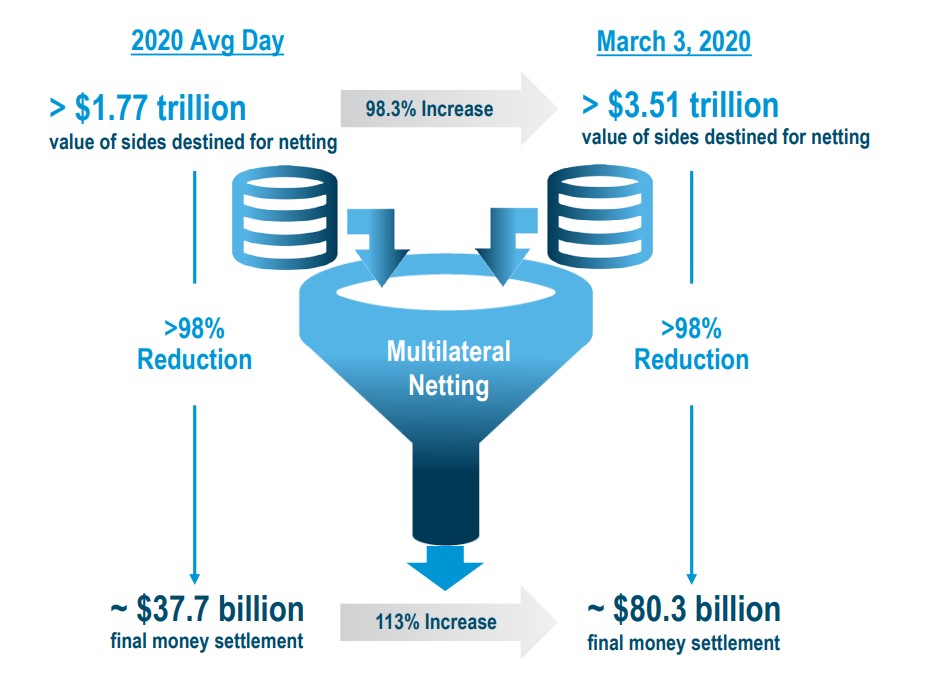

This happens at scale through clearinghouses like the Depository Trust & Clearing Corporation, which act as central counterparties that net obligations and manage settlement risk. As a result, financial systems can compress large volumes of transactions into much smaller net flows.

Before central banks, merchants at European trade fairs settled debts by netting obligations across multiple parties, reducing the need to move physical money. Over time, these practices evolved into more formal clearing systems.

Buchman also pointed to later experiments in Yugoslavia and Slovenia as examples of multilateral netting at scale.

Related: Prediction markets are testing legal limits in strict Asian markets

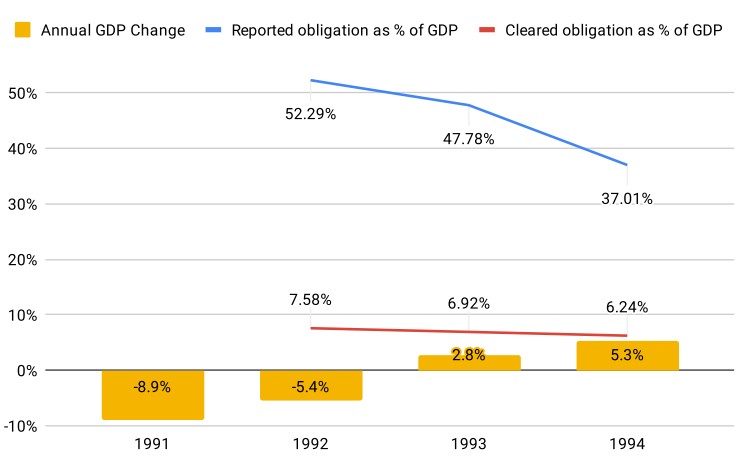

Following independence in 1991, Slovenia turned to multilateral set-off systems to manage liquidity during periods of economic stress. As inflation surged and output contracted, authorities used centralized payment infrastructure to coordinate obligations across firms, netting debts before settlement.

The system, later formalized through software known as “TETRIS,” applied liquidity-saving mechanisms to reduce how much capital needed to move, helping businesses continue operating despite widespread payment constraints.

Crypto’s instant settlement locks up liquidity

Instead of designing systems that batch and net obligations, most crypto markets are built around instant, atomic settlement, where each transaction is finalized independently.

For example, put simply, if Alice sends 10 ETH to Bob for a trade, that transfer is fully settled onchain at execution. If Bob later owes Alice 9 ETH from another trade, that is processed as a separate transaction rather than being netted against the first. Instead of settling a 1 ETH difference, the system processes 19 ETH of transfers across two transactions.

Across many trades, this forces participants to continuously move and pre-fund capital, even when their net exposure is close to flat.

“That means you need way more capital in the system than you otherwise would,” Buchman said.

Instant settlement removes counterparty risk, but it also removes the ability to offset positions across a broader network of participants. That compression layer is largely missing in crypto, which means more capital is required to support the same level of activity.

Related: Ethereum’s EEZ and the attempt to rebuild one Ethereum

“There is a kind of ceiling on how much trade you can do, depending on how much actual assets and capital you have to meet it,” Buchman said.

“A lot of the firms are doing a lot of trading on credit with each other, but then when it comes time for settlement, they have to scramble for the assets,” he said.

That forces crypto companies to overcollateralize positions on exchanges and lending platforms, tying up capital that could otherwise be deployed elsewhere. In periods of stress, the problem becomes more acute, as firms are left trying to meet settlement obligations while liquidity tightens.

The missing primitive is clearing, now being rebuilt without intermediaries

Replicating clearing in its traditional form requires building a central counterparty. The model may sit uneasily with an industry aiming to replace financial intermediaries with decentralized infrastructure.

Clearing entities are among the most heavily regulated and trust-intensive institutions in finance, Buchman said. They absorb default risk, stand between participants and require deep coordination to function.

Crypto avoided that model and instead fragmented clearing. Bilateral arrangements and off-exchange settlement venues introduced limited netting, but mostly within closed networks of trust, leaving the core problem unresolved.

Buchman and Cycles propose a coordination layer that nets obligations across participants before settlement, without acting as a central counterparty or taking custody of funds.

Its effectiveness, however, depends on broad participation and visibility into obligations, which may be difficult to achieve in a fragmented market where firms operate across venues and are reluctant to share exposures. Without a central counterparty, the system also does not absorb default risk, leaving participants to manage counterparty exposure themselves.

Coordinating multilateral netting across independent actors could also introduce operational complexity, particularly during periods of market stress when liquidity is already constrained.

Buchman argues this can be addressed using cryptographic techniques, with obligations posted privately onchain, netted in software and verified using zero-knowledge proofs.

In that sense, the trade-off for crypto is that trust in an institution is replaced by trust in the protocol’s design.

Magazine: ‘Phantom Bitcoin’ checks, Drift hack linked to North Korea: Asia Express