The key constraint on real-world assets (RWAs) has been regulatory engagement rather than technology, and that dynamic has been shifting in the US, said Ashley Ebersole, chief legal officer of Sologenic.

Ebersole joined the Securities and Exchange Commission (SEC) in early 2015, where he served in the agency’s early internal working groups on crypto and the application of securities law to blockchain-based assets.

The securities regulator published the DAO Report in 2017, asserting its jurisdiction over tokens that met the definition of securities. What followed was an enforcement-led approach that left little room for sustained dialogue with the industry.

“After the DAO Report, it was an enforcement response for the next two years. I expected there would be more of a rotation toward policy while I was still there — that didn’t happen,” he told Cointelegraph.

Ebersole said that posture hardened after he left the agency, shortly before Gary Gensler took the helm in April 2021. From private practice, he continued engaging with the SEC until staff were later discouraged from interacting with crypto firms.

The communication breakdown made it difficult for companies to design legally compliant RWA products and delayed the development of onchain securities models that are now moving into production.

How compliant RWAs can work in practice

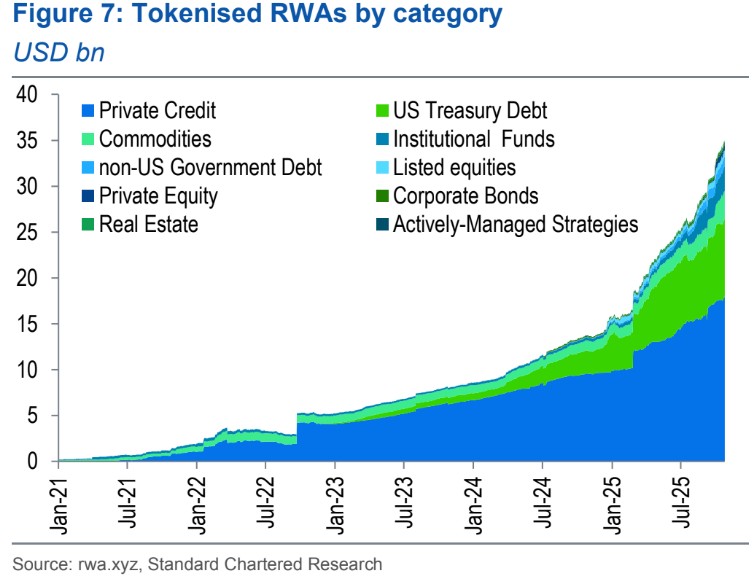

The market for tokenized real-world assets is scaling quickly. Standard Chartered has projected that the value of non-stablecoin RWAs could reach $2 trillion by 2028, driven largely by tokenized equities, funds and other traditional financial instruments migrating onto blockchains.

Major financial institutions are positioning for that shift. BlackRock is reportedly exploring tokenization to modernize fund infrastructure, while JPMorgan has launched tokenized money-market products on Ethereum.

“There is a right way to do compliant tokenization and issue tokenized assets. It absolutely can be done,” Ebersole said.

Related: Ronin and ZKsync’s onchain metrics fell the most in 2025

One model he pointed to involves stock tokens that function similarly to depository receipts. When a user purchases a token, a corresponding share is acquired and held by a regulated clearing broker, while a token is minted to represent contractual rights to that share.

“You own it. It’s minted at the time of purchase, and it references contractual rights to a share of stock that was purchased at the same time,” Ebersole said.

“And you get the dividends and the voting rights and everything else that comes with being a shareholder, because you are.”

Ebersole said this approach differs from other tokenized stock products that offer price exposure without conferring ownership. In those cases, stock tokens function as synthetic instruments that track the price of an equity without granting shareholder rights or a legal claim on the underlying asset.

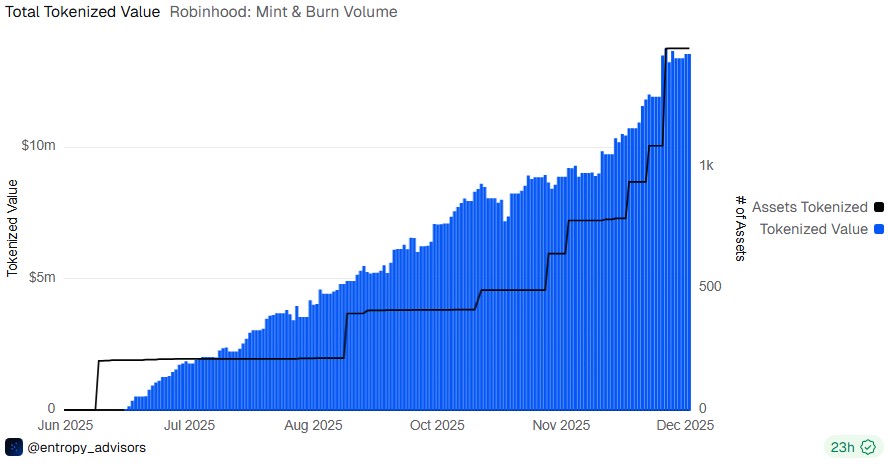

The distinction remains relevant today. In late July, Robinhood promoted tokenized exposure linked to OpenAI. The private company publicly distanced itself from the product and said that any transfer of its equity requires approval, which did not occur.

Where RWA tokenization breaks down

Interest in tokenized RWAs is accelerating, but Ebersole warned that it does not eliminate the geographical constraints of securities regulation. In practice, many RWA initiatives run into legal and jurisdictional limits.

Securities laws remain nationally bound even if blockchain infrastructure is not. An RWA structure that complies with US requirements does not automatically translate to the European Union or Asian markets, where separate licensing, disclosure and distribution rules apply.

“The toughest thing we hear about with tokenized RWA projects is the maze of legal requirements that apply to these assets if you’re doing them in a fully legally compliant way,” Ebersole said. “That’s true in the US, and it’s even more complicated globally.”

Related: How crypto is used in 2025: YouTube, Pokémon cards and more

That fragmentation has pushed many platforms toward region-specific offerings. Robinhood’s tokenization offering is limited to EU users. It allows trading in tokenized US stocks and exchange-traded products but does not confer direct ownership of the underlying shares. Instead, the tokens mirror the prices of publicly traded securities and are regulated as blockchain-based derivatives under the bloc’s Markets in Financial Instruments Directive II (MiFID II).

Yield is another area where RWA tokenization often runs into regulatory friction. Ebersole noted that regulators draw a sharp distinction between yield generated through a holder’s own actions — such as participating in transaction validation — and yield that accrues passively simply by holding a token.

“If you buy an asset with an inherent yield just by virtue of holding it, regulators are still going to look at that as the hallmark of a security,” he said.

That distinction has already shaped enforcement decisions and continues to influence how tokenized products are structured. While regulatory views on staking and other forms of yield have evolved under the current SEC administration, Ebersole said inherent yield remains a sensitive trigger under current law.

The regulatory shift behind RWA momentum

The practical shift for RWAs has come from a change in how the SEC approaches the industry. During an enforcement-heavy period under the Gensler-led SEC, when staff were discouraged from engaging with crypto firms, would-be issuers were left without a workable path to build compliant onchain products, even when attempting to operate within existing securities law.

That posture has begun to soften as the agency signals greater openness to engagement. Ebersole pointed to recent leadership changes at the SEC, including the arrival of Paul Atkins, as contributing to a tone that treats blockchain technology as infrastructure with potential applications for securities markets rather than as an inherent regulatory risk.

“Now the SEC is engaging a lot with the industry and saying, ‘Come in and tell us if you are trying to do what we’re trying to do, how would you do it?’” Ebersole said.

In that environment, compliant models such as tokenized equities structured through regulated intermediaries and custody arrangements can move from concept to production, even as legal friction persists around cross-border distribution and yield-bearing designs that can still trigger additional securities obligations.

Existing securities law continues to govern RWAs, but the move away from an enforcement-only posture does not, in Ebersole’s view, foreclose the possibility of more tailored rules over time if regulators and the market continue working through remaining gaps.

Magazine: Big questions: Would Bitcoin survive a 10-year power outage?